Proposal description

Earn Dash on Your Savings Account!

This is a proposal to expand Dash liquidity, increase awareness, and drive adoption. Users can earn over 10% interest annually and payable in Dash.

Overview

Genitrust Savings users earn over 10% yearly interest. Next: Genitrust Savings will give their users the ability to earn their interest on their savings account not only in US Dollar, but now in Dash. This proposal outlines a method, partnership, and technology that Genitrust will employ to both help end Dash users, and get Dash in the hands of your average person and your average business – drastically increasing Dash’s reach in the US and other markets.

The primary vehicle for doing this will be a partnership with Genitrust Savings, which – through a Hyper-Yield Savings Account, will allow virtually everyone in the United States, to immediately earn over 10% on their savings, while at the same time, paying out the interest earnings in DASH. This can potentially get millions of new people utilizing DASH and the DASH Network.

Today, people are intrigued by Cryptocurrency. From listening to nearly a decade of tech and investing news cycles, the majority of people understand the basic principles and are curious about the technology. They do not want to be left out, and even today they still struggle to participate and see what Dash is all about. They do not know where to start, still! And we can change that.

Genitrust recognizes that the current on-ramps are complicated, time-consuming, and are built using conventional “broker-account” methodologies, which places these services out of reach to the average consumer. Evidence of this is the recent report from Mizuho Securities given to CoinDesk that nearly 20% of PayPal users have already traded bitcoin using PayPal’s mobile app (https://finance.yahoo.com/news/almost-20-paypal-users-used-185507472.html).

What better way to drive adoption then through a vehicle that will help account-holders earn DASH interest payments on their savings?

Genitrust’s History

About Genitrust

In the beginning, Genitrust’s Savings system worked similarly to a CD (investors had to deposit a significant amount of cash) and they were locked into a 1-year contract. In 2020, Genitrust released “Genitrust Savings” to the public, allowing anyone to save and earn hyper-yield interest with no minimum deposit, no fees, and access to their money at any time.

(Genitrust Savings: https://genitrust.com)

Today, Genitrust Savings has continued to grow exponentially with an average month-on-month growth of 300% since release! The average Genitrust Savings member earns over 10% annual interest with NO investment risk.

Over the years, Genitrust has worked with private investors and provided amazing returns with little risk. How does Genitrust drive returns? By providing liquidity to peer-to-peer exchanges and realizing a profit for every transaction. This drives profit for Genitrust investors, stake-holders, and account holders, as well as helps to drive cryptocurrency adoption. This activity, and Genitrust’s previous work in the DASH and cryptocurrency space, has already made large positive impacts on both crypto adoption as well as DASH’s price. For example, when Genitrust first worked with Dash in early 2017, Genitrust was able to put strong buying pressure on institutional markets, causing the price of Dash to rise from $12 to about $60 before Dash’s integration announcement with its first major exchange (Bitfinex). (Source: https://cointelegraph.com/news/wall-of-coins-integrates-dash-as-it-surges-to-number-3-cryptocurrency-all-time-highs)

What does Genitrust envision to be beneficial for Dash and Humanity?

Genitrust seeks to be a leader in the USA for opening up new, but conventional customers and clients to Dash. At our core, we believe in Dash. Like language, or thought, users of money are constantly looking for “instant” solutions that enable unrestricted, global, financial freedom. The company founders have been involved in Crypto since the earliest days, spent time building successful companies, and developed numerous relationships in the Crypto sphere.

Genitrust understands the intricacy, security, legal, philosophical, ethical, and monetary-safety concerns (and the implications of these new technologies) on existing structures as well as the pros and cons of virtually every major Crypto in the space. It is with this context and understanding that we know Dash is the best financial tool today for the world we’re entering, with one glaring speed bump – more users need to know about and have easy access to Dash. This proposal explains the technology and underlying business structure outlined in this partnership that will smooth out this speed bump and increase Dash’s brand awareness, liquidity, user-base, and ultimately price.

Itemized ROI for the Dash Community and Stakeholders:

First, upon approval of this proposal, we will allow our existing and future customers to elect to receive a portion (or all) of their interest earnings in Dash instead of US Dollar. We will educate users that buying $1 of Dash per day throughout a 2 year period resulted in tripling their money. (Dollar cost averaging purchases = awesome.)

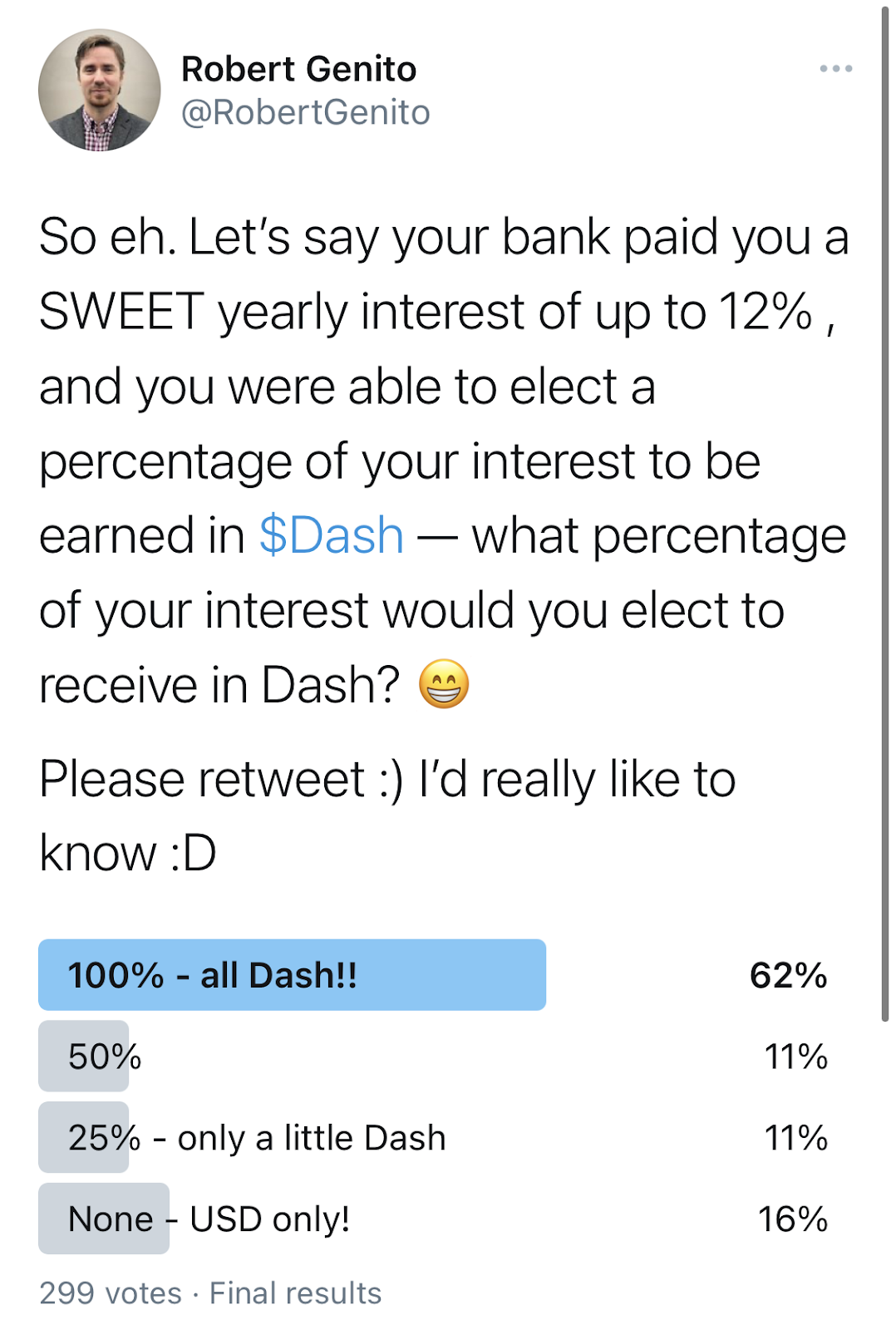

Below, you can see a tweet from CEO Robert Genito polling users on what portion of their interest they would elect to receive in Dash.

Budget

200 DASH.

This is for the technology development, user experience research and design, inclusion of Dash in future marketing, and solid execution of this campaign. We believe it will take us at least 400 human hours to complete this project plus 15% extra time to handle unexpected matters, the first couple of weeks of UX adjustments, and an ongoing evaluation of effectively communicating the value proposition to new users.

What if 200 DASH is not enough? Only if we must, we may ask the network for extra allowance. We do not anticipate this happening, and we mention this for the benefit of full transparency.

What if 200 DASH is too much of a budget? We have many future proposals in mind, and we will discount future proposals by the overage budget that we have.

What can we guarantee?

We anticipate finishing and deploying this project within 30 to 35 business days. The extra 5 days will cover any unexpected events such as staff sickness or unexpected necessary development. We see the release date for this feature to be either the late evening of February 9th (Tuesday) or February 10th (Wednesday).

The week of Dec. 28th:

Genitrust Savings is currently available for people who have a US-based mobile phone number. No deposit is necessary to have an account, there are no fees, and users can withdraw their money any time. Sign up here using promo code “Dash OG”, and if you do make a deposit, you will get a promotional bonus of 2% on your first deposit. Imagine that bonus giving you Dash instead of USD!

Web App: https://genitrust.com

iPhone: https://geni.to/ios

Android: https://geni.to/android

This is a proposal to expand Dash liquidity, increase awareness, and drive adoption. Users can earn over 10% interest annually and payable in Dash.

Overview

Genitrust Savings users earn over 10% yearly interest. Next: Genitrust Savings will give their users the ability to earn their interest on their savings account not only in US Dollar, but now in Dash. This proposal outlines a method, partnership, and technology that Genitrust will employ to both help end Dash users, and get Dash in the hands of your average person and your average business – drastically increasing Dash’s reach in the US and other markets.

The primary vehicle for doing this will be a partnership with Genitrust Savings, which – through a Hyper-Yield Savings Account, will allow virtually everyone in the United States, to immediately earn over 10% on their savings, while at the same time, paying out the interest earnings in DASH. This can potentially get millions of new people utilizing DASH and the DASH Network.

Today, people are intrigued by Cryptocurrency. From listening to nearly a decade of tech and investing news cycles, the majority of people understand the basic principles and are curious about the technology. They do not want to be left out, and even today they still struggle to participate and see what Dash is all about. They do not know where to start, still! And we can change that.

Genitrust recognizes that the current on-ramps are complicated, time-consuming, and are built using conventional “broker-account” methodologies, which places these services out of reach to the average consumer. Evidence of this is the recent report from Mizuho Securities given to CoinDesk that nearly 20% of PayPal users have already traded bitcoin using PayPal’s mobile app (https://finance.yahoo.com/news/almost-20-paypal-users-used-185507472.html).

What better way to drive adoption then through a vehicle that will help account-holders earn DASH interest payments on their savings?

Genitrust’s History

About Genitrust

In the beginning, Genitrust’s Savings system worked similarly to a CD (investors had to deposit a significant amount of cash) and they were locked into a 1-year contract. In 2020, Genitrust released “Genitrust Savings” to the public, allowing anyone to save and earn hyper-yield interest with no minimum deposit, no fees, and access to their money at any time.

(Genitrust Savings: https://genitrust.com)

Today, Genitrust Savings has continued to grow exponentially with an average month-on-month growth of 300% since release! The average Genitrust Savings member earns over 10% annual interest with NO investment risk.

Over the years, Genitrust has worked with private investors and provided amazing returns with little risk. How does Genitrust drive returns? By providing liquidity to peer-to-peer exchanges and realizing a profit for every transaction. This drives profit for Genitrust investors, stake-holders, and account holders, as well as helps to drive cryptocurrency adoption. This activity, and Genitrust’s previous work in the DASH and cryptocurrency space, has already made large positive impacts on both crypto adoption as well as DASH’s price. For example, when Genitrust first worked with Dash in early 2017, Genitrust was able to put strong buying pressure on institutional markets, causing the price of Dash to rise from $12 to about $60 before Dash’s integration announcement with its first major exchange (Bitfinex). (Source: https://cointelegraph.com/news/wall-of-coins-integrates-dash-as-it-surges-to-number-3-cryptocurrency-all-time-highs)

What does Genitrust envision to be beneficial for Dash and Humanity?

Genitrust seeks to be a leader in the USA for opening up new, but conventional customers and clients to Dash. At our core, we believe in Dash. Like language, or thought, users of money are constantly looking for “instant” solutions that enable unrestricted, global, financial freedom. The company founders have been involved in Crypto since the earliest days, spent time building successful companies, and developed numerous relationships in the Crypto sphere.

Genitrust understands the intricacy, security, legal, philosophical, ethical, and monetary-safety concerns (and the implications of these new technologies) on existing structures as well as the pros and cons of virtually every major Crypto in the space. It is with this context and understanding that we know Dash is the best financial tool today for the world we’re entering, with one glaring speed bump – more users need to know about and have easy access to Dash. This proposal explains the technology and underlying business structure outlined in this partnership that will smooth out this speed bump and increase Dash’s brand awareness, liquidity, user-base, and ultimately price.

Itemized ROI for the Dash Community and Stakeholders:

- “Free” Dash - Savers and Independent Contractors will receive their first Dash, something they did not have to purchase or work for, yet something they still value because they had given up interest earnings in exchange for owning Dash.

- “Safer” Investing - With traditional crypto investing, the users must risk their principle to earn a return. This solution allows users to gain exposure to crypto without risking their base investment, and thus potentially access users that are hesitant about crypto price volatility.

- Education & Brand Awareness - Independent Contractors and Small Businesses will learn the basics of Dash.

- Easily Spend Dash - They will also realize that they can use Dash for spending, further speculation, and an inflation-proof sovereign money – and spend it directly from their wallet, or move it to another more personal wallet.

- Exclusive Partnership & Marketing Opportunity - Dash will receive an exclusive partnership during the first month of deployment. Our system upgrades, and proposed marketing will highlight Genitrust Savings & Dash’s relationship and be spread across both Crypto-related and more general tech news outlets, helping to further expand Dash’s reach and awareness. Customers will be able to realize their interest in Dash and not the plethora of other blockchain assets and cryptocurrencies dying to have this sort of airdrop functionality.

- Develop On-ramps for Other Large Companies – We see the opportunity for large companies such as PayPal, Cash App, and Venmo to integrate Dash in a similar manner to Genitrust Savings. Our partnership will shine as a beacon to other banks, savings tools, wallets, and payment platforms to follow suit. We’ll be able to consult with the Dash community and be a liaison for any such business relationships after launch (both technically, as well as from a testimonial perspective). This will help these larger entities understand the value in implementing Dash in their platforms.

- Improve Liquidity and Adoption – Post-launch, the Genitrust Savings partnership will continue to improve Dash liquidity, adoption, and public awareness in the USA. From this feature implementation, this can open up many more possibilities.

- A: Imagine being able to have the world’s first “Dash Savings” account that accrues interest, and imagine the example and influence it will have on disrupreneurs (entrepreneurs + disrupters) to bring Dash’s decentralized vision to humanity.

- B: Dash’s First Fiat On-ramp with a familiar “bank-like” interface: get Dash by direct bank account transfer, debit cards, and credit cards.

- C: Spend Dash on a local-currency settled debit card.

- D: Imagine the USA’s citizens who wish to exodus the US Dollar having a simple solution to export exclusively to Dash.

- New users that are recent crypto adopters

- More wallet downloads

- Greater liquidity

- Greater interest in Dash’s innovations from larger “bank-like” companies

First, upon approval of this proposal, we will allow our existing and future customers to elect to receive a portion (or all) of their interest earnings in Dash instead of US Dollar. We will educate users that buying $1 of Dash per day throughout a 2 year period resulted in tripling their money. (Dollar cost averaging purchases = awesome.)

Below, you can see a tweet from CEO Robert Genito polling users on what portion of their interest they would elect to receive in Dash.

Budget

200 DASH.

This is for the technology development, user experience research and design, inclusion of Dash in future marketing, and solid execution of this campaign. We believe it will take us at least 400 human hours to complete this project plus 15% extra time to handle unexpected matters, the first couple of weeks of UX adjustments, and an ongoing evaluation of effectively communicating the value proposition to new users.

What if 200 DASH is not enough? Only if we must, we may ask the network for extra allowance. We do not anticipate this happening, and we mention this for the benefit of full transparency.

What if 200 DASH is too much of a budget? We have many future proposals in mind, and we will discount future proposals by the overage budget that we have.

What can we guarantee?

- All Genitrust Savings users now and in the future will learn why receiving all (or some) of their interest in Dash is beneficial.

- We can guarantee the release timeline for these features going live is accurate. See the timeline, below.

- All applicable Dash-related technologies that can be modularized will be provided as open source, and available directly from Genitrust.com, so that other companies can utilize our technology to connect Dash to their website.

We anticipate finishing and deploying this project within 30 to 35 business days. The extra 5 days will cover any unexpected events such as staff sickness or unexpected necessary development. We see the release date for this feature to be either the late evening of February 9th (Tuesday) or February 10th (Wednesday).

The week of Dec. 28th:

- Genitrust begins designing the UX and writing up tech specifications on precisely how this will be implemented in Genitrust Savings.

- A focus will be put on how these tech items can be created modular-enough to become useful for other companies using a similar tech stack as Genitrust.

- The first draft of company backend policies and procedures will be drafted and discussed. These new policies and procedures will complete how the company will issue Dash to account holders, how the company will acquire Dash, and how the company will secure the end user’s interest holdings.

- This information will be packaged for our banking and exchange partners to understand what we are doing.

- By this time, the first UX mockups will be approved and the UI/UX technical implementation will begin.

- The backend database models will be drafted and first implemented by software unit tests.

- Any potential issues with the initial plan will be re-evaluated and mitigated.

- By the end of the week, we can anticipate having at least 2 exchange partners on board with the business. The goal is to have our exchange partners understand the continued brilliance, resiliency, and opportunity of supporting the Dash ecosystem’s continual growth, just as we had communicated in early 2017 when Genitrust worked with Dash.

- UX/UI development will be secured by Behavioral Driven Unit Tests to ensure future developments do not break the user’s experience and to speed up the Quality Assurance testing.

- By the end of this week, all Unit Tests will be finished, and the technological implementation that will connect the backend and the front end will be of heavy focus.

- All UI and backend development must be completed by the team and ready for QA testing next week.

- During this time, a knowledge base and “quick guide” manual will be drafted to communicate with the backend finance ops staff on how to perform the necessary work for rewarding customers with Dash Interest. We can only anticipate the most common problems and how the team will go about solving unexpected issues with real-world business activities.

- Genitrust’s Marketing Officer will begin a kick off meeting on how the Dash Interest campaign will be communicated with existing and new users, and what materials will be developed for the announcement.

- Quality Assurance (QA) testing begins this week, as well as software fixes and other necessary behavioral and unit tests.

- The tools necessary for the finance operations department will be implemented and finished this week.

- System Operations will have any necessary systems up-and-running within the company’s policies — e.g. the Dash Insights server, the company cold storage Dash wallet for these purposes, etc.

- If QA is not complete this week, we will discuss the best strategy to have this feature in production on time.

- Finance Operations staff will be trained on how to work with all Dash-related matters and company policies.

- Integration testing begins and the production release will be approved for Tuesday evening.

- Genitrust will discuss with Dash Masternodes owners and respected community members about the marketing materials for feedback.

- The software feature will be in production and available on https://genitrust.com and the Genitrust Savings app for Android and iOS.

- Genitrust’s Dash Interest marketing campaign begins.

Genitrust Savings is currently available for people who have a US-based mobile phone number. No deposit is necessary to have an account, there are no fees, and users can withdraw their money any time. Sign up here using promo code “Dash OG”, and if you do make a deposit, you will get a promotional bonus of 2% on your first deposit. Imagine that bonus giving you Dash instead of USD!

Web App: https://genitrust.com

iPhone: https://geni.to/ios

Android: https://geni.to/android

Show full description ...

Discussion: Should we fund this proposal?

Submit comment

Would it be possible for you to approach the Dash Investment Foundation and see if they would be willing to float a proposal on your behalf? The DIF supervisor can sign an NDA. If you can convince them that this offer truly makes sense for the DAO, you will probably get your funding.

Plus, this feature is a great alternative for:

— Dash newcomers can passively earn Dash. This gives them the opportunity to actually use Dash in the real world and experience the benefits and overall excitement. This is something you cannot communicate to someone with words, and people really don’t care to download a wallet when they don’t need to (because they do not have Dash in the first place, nor do they want to buy it…). There is no better way to understand the novelty of Dash than by having Dash to use for oneself. What other companies are doing this? None.

— Dash enthusiasts have an additional way to earn Dash on savings that they’re using to pay for a personal emergency, to buy a special present, to put down money on a new car, etc.

In these times, services like Genitrust Savings are in high demand. The customer base is growing quickly, and this growth will continue to accelerate as people gain more confidence. Dash’s ecosystem (and price) has a lot to gain by exclusively being part of Genitrust Savings early.

We need a good look at Genitrust's operations, specifically exactly how the generous returns promised to users are generated. We need assurances that we are not dealing with a mini-madoff who needs money make good on those promises.

Btw, are you aware that Genitrust has more reputation and proven past success than *most* passing proposals ever?

Genitrust's first proposal (4 years ago today) was high risk yet yielded a massive success for Dash adoption and development: https://cointelegraph.com/news/wall-of-coins-integrates-dash-as-it-surges-to-number-3-cryptocurrency-all-time-highs

The proposal we do today is a relatively inexpensive proposal that I would consider to have little short-term risk for a promising yield with an established, thriving business, and it opens Dash up for inclusion on a new developing service that many people are excited about. Genitrust has the knowledge, experience, and execution mastery to bring Dash along with its success and do this again and again for the Dash ecosystem, but we can only do this when the voting community's desire for success is greater than the fear of failure.

Thank you for truly being the devil's advocate here and bringing up very valid concerns.